A Better Understanding of Economics, Personal Finance Education, and Economic Inequality

The Current Landscape of Economics and Personal Finance Education in the United States

The need for greater financial literacy among Americans of all ages and backgrounds has become a hot topic for stakeholders, parents, and educators in recent decades. Studies have shown that many adults lack basic knowledge about personal finance, including banking, credit, debt management, and savings. The Personal Finance Index from the Teachers Insurance and Annuity Association (TIAA) Institute and the Global Financial Literacy Excellence Center (GFLEC) at George Washington University assesses the financial literacy of U.S. adults. The 2022 results indicated that, on average, respondents correctly answered only 50 percent of the questions, with 18 percent of respondents correctly answering more than 75 percent of the questions and 23 percent of respondents correctly answering 25 percent or fewer of the questions. Results also showed that respondents who had fewer correct answers were more likely to experience financial difficulties, including high debt levels, lack of savings, and living paycheck-to-paycheck.

The 2021 National Financial Capabilities Survey (NFCS), conducted by the Financial Industry Regulatory Authority Foundation (FINRA), found that respondents with low financial literacy were more likely to spend more money than their income, less likely to set aside emergency funds, and less likely to have a retirement plan or retirement account compared to respondents with high financial literacy. Additionally, the survey revealed that respondents with low financial literacy were more likely to incur late payment fees, use credit cards for cash advances, exceed credit limits, and borrow money from non-banking institutions, such as pawn shops or ‘pay-day’ loan businesses.

In 2018, Junior Achievement surveyed 1,000 teenagers between the ages of 13 and 18 years old about their understanding of personal finance. Ninety-five percent of respondents agreed that taking a personal finance class during high school would be valuable. When asked about future personal financial concerns, 54 percent of respondents indicated paying for college, followed by 52 percent not being able to find a well-paying job, 49 percent not being able to afford a home, 43 percent not having the necessary skills to manage money, and 42 percent not being able to save money for an emergency.

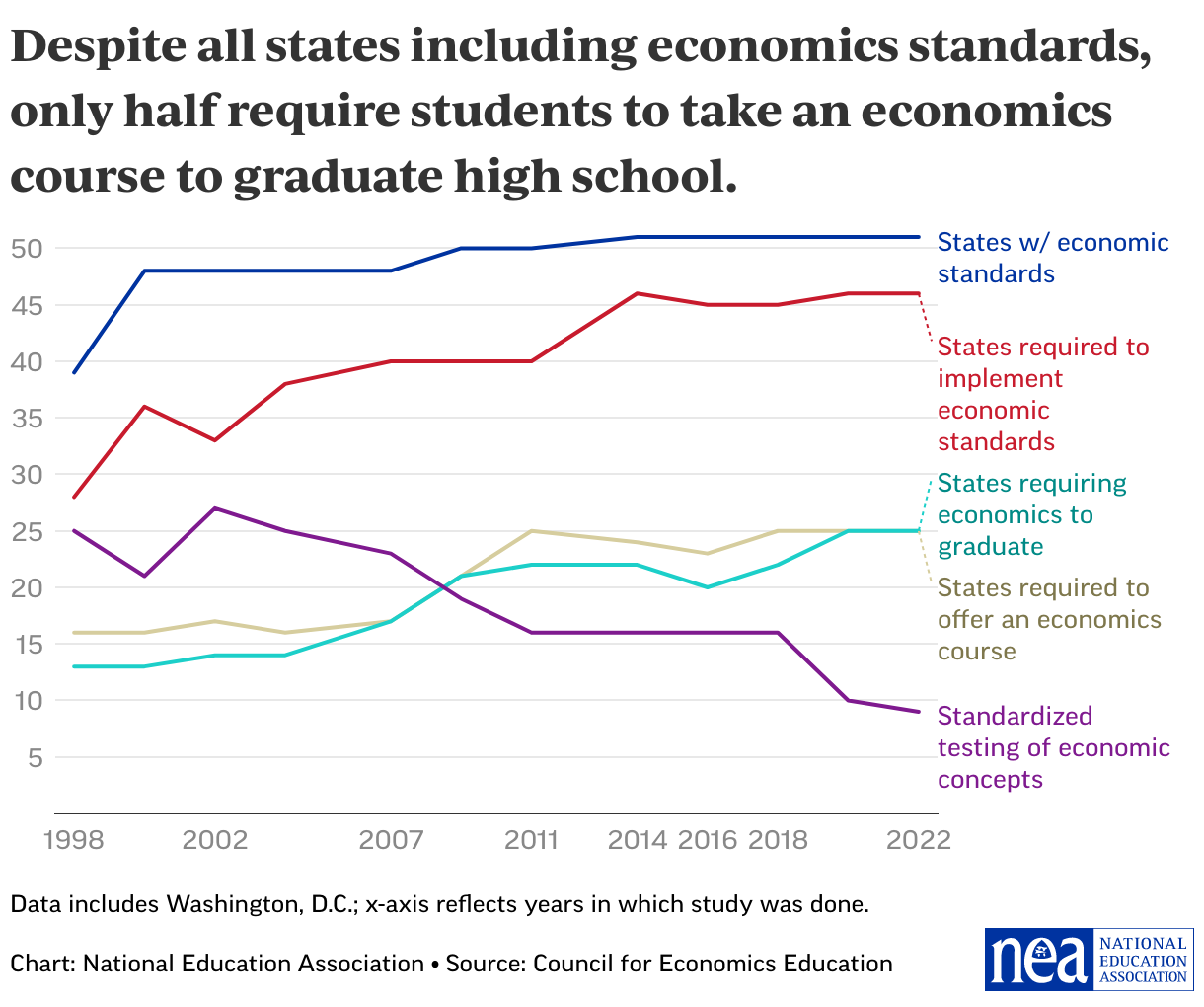

Based on these studies, it is evident that there is not only a need but also a desire for financial literacy instruction in schools. A report from the Council for Economic Education (CEE) found that although all 50 states plus Washington, D.C., included economics in their K–12 social studies standards, only 25 states required students to complete an economics class to graduate high school as of 2022. This requirement has remained relatively unchanged since 2011 and has only increased by nine states since 1998.

Section with embed

Between 1998 and 2022, the number of states that included personal finance in their K–12 social studies standards increased from 21 to 47. During the same period, the number of states that required personal finance to graduate increased from 1 to 23.

Increasingly, stakeholders and politicians are calling for personal finance instruction in K–12 schools. During their 2021 legislative sessions, 38 states; Washington, D.C.; and Puerto Rico introduced legislation addressing financial literacy. Thirty-seven states plus Washington, D.C.; Guam; and Puerto Rico introduced financial literacy legislation the following year.

Across state legislatures, personal finance standards have garnered bipartisan support. For example, Republican Senator Chris Gebhard, who sponsored a bill requiring a personal finance course to graduate from Pennsylvania public schools, said that “by teaching high school students the financial basics, they will learn necessary money management skills to position themselves for lifetime success and financial independence.” Additionally, Democratic Senators Antonio Maestas and Michael Padilla of New Mexico are cosponsoring a similar bill in their home state, making personal finance a required course for all high school students. In June 2022, Democratic Governor Gretchen Whitmer signed HB 5190 into law—a bipartisan bill introduced by Republican Diana Farrington that requires financial literacy instruction in Michigan’s public schools.

In recent decades, researchers have turned their attention to the effectiveness of economics and personal finance education taught in K–12 schools. Research reviews find that teaching personal finance in schools has a positive effect on students’ financial literacy and economic behavior.

A 2022 study conducted in Georgia and Texas found that students who received personal finance instruction had higher credit scores and were less likely to be delinquent on credit card payments. Over the course of the study in Georgia, student credit scores increased by 7 points for the first cohort, 18 points for the second cohort, and nearly 27 points for the third cohort. The Texas cohorts showed similar results.

Although research has shown positive outcomes for students receiving financial literacy instruction, there are glaring gaps that need further study. Discussion of ethnicity, gender, race, and sexuality is largely absent from these studies. Stakeholders and politicians have latched on to positive student outcomes arguing that financial literacy education is the solution for closing persistent wage gaps and economic disparities in the United States. Arguably, financial literacy can benefit any student, but it is necessary that the curriculum and standards address contemporary and historical economic injustices that have perpetuated disparities in housing, employment, wages, and banking.

The National Education Association supports personal finance instruction and standards to “help students gain the financial literacy skills they’ll need to manage their financial resources effectively throughout their lives.” The NEA provides personal finance resources, including standards, lesson plans, teaching materials, and games, which can be found through the following links:

The NEA supports the adoption of the National Standards for Personal Financial Education created by the Jump$tart Coalition and the Council for Economics Education. These standards provide educators with a “framework for a complete personal finance curriculum” designed for students from elementary through high school. The standards include topics on earning income, spending, saving, investing, credit, and managing risk. Additionally, these standards address economic inequity, including topics on race and gender wage gaps, discrimination in borrowing, and economic and employment experiences based on ethnicity and gender.

It is the purpose of this work to aid the promotion of honesty in education by providing information and resources about the need to amend or establish economics and personal finance standards due to historical reasons that exacerbated economic disparities in the United States. Having a full and honest financial curriculum will foster critical thinking and an understanding of the foundational causes of economic disparities based on race and gender and will promote the need to dismantle the systems of instructional racism that have continued to impact and perpetuate the wealth disparities in our country. Specifically, we provide data and resources regarding discriminatory practices and policies in housing, education, employment, and banking that have hindered the economic progress of Native People, People of Color, women, and LGBTQ+ individuals.

Additionally, we highlight actions that must be taken to help address economic inequities in the United States. More specifically, we must focus on closing racial income gaps. A 2019 study by researchers at the Cleveland Federal Reserve Bank concluded that “policies designed to speed the closing of the racial wealth gap would do well to focus on closing the racial income gap.” The persistence of the Black-White wealth gap, they found, is nearly entirely due to the persistence of the income gap between Black and White workers. It turns out that the impact of other factors often cited, including inheritances and success in investments, are far less important than the straightforward gaps in income.

While we examine the various ways in which racial and gender discrimination manifest in our economy—gaps in educational attainment, income, housing and other assets, and wealth—we must also strive to fix the underlying problems. Gaining financial literacy is a necessary and valuable resource as well as a lifelong skill but it is ultimately the government that must use its powers to shape and enforce policies, laws, and regulations to make meaningful headway in dismantling the structures that create and perpetuate racial and gender discrimination in our society.

The government can do several things to increase worker wages in an equitable way:

- Make entry-level jobs pay a living wage by raising the federal minimum wage, which has remained unchanged since 2009 at $7.25. In 2023 dollars, that is equal to just $5.15.

- Strengthen and enforce labor protections for workers by enforcing wage laws to crack down on rampant ‘wage theft’—when employers cheat employees of wages they’ve earned—and strengthening laws to protect ‘gig’ workers who are easily exploited. We must advocate for regulation changes to make it less onerous for workers to prove charges of unfair practices by employers.

- Enlist the Federal Reserve Board in the effort for equality. This proposal was enacted by Congress in 2022, when they called on the Federal Reserve Board to take specific steps to foster "the elimination of disparities across racial and ethnic groups with respect to employment, income, wealth and access to affordable credit." An earlier analysis by researchers from the Richmond Federal Reserve Bank and University of California–San Diego also found that this could indeed help to improve economic well-being for Black households.

- Better job training. A small levy on large corporations could fund a national trust that would facilitate modern job training programs to specifically prepare trainees for high-quality jobs.

- Make the job application process fairer. Through the implementation of ‘Ban the Box’ (as discussed in a report by the Center of American Progress and a toolkit from the National Employment Law Project), we would eliminate questions (or check boxes) regarding criminal convictions on application forms and use ‘blind applications,’ which don’t ask for individually identifying information. Also, by upgrading background check data systems, we would avoid mislabeling applicants as criminals.

- Raise incomes for the workers, raise taxes on the rich. This ‘big picture’ recommendation from Nick Hanauer in his Atlantic article “Better Schools Won’t Fix America,” he makes the case that ‘educationism’—the notion that education alone can fix all of society’s economic and social shortcomings—is well-entrenched because it makes the wealthy feel good about not sharing their wealth or power. What is needed, he argues, is to simply pay workers more: Besides raising the minimum wage and restoring labor’s bargaining power that was largely lost beginning in the 1980s, he calls for reinstituting the progressive tax rates on the rich that were in effect for decades and were substantially responsible for building the strong middle-class society characteristic of the 1950s–1970s. Hanauer goes on to say, “We have confused a symptom—educational inequality—with the underlying disease: economic inequality. Schooling may boost the prospects of individual workers, but it doesn’t change the core problem, which is that the bottom 90 percent is divvying up a shrinking share of the national wealth. Fixing that problem will require wealthy people to not merely give more, but take less.”

Financial literacy courses create awareness of the historical roots and causes of how gaps in educational attainment, employment, income, home ownership, and other components of the quality of life were borne into existence. These courses can give students valuable tools they can use to improve their own personal circumstances as they enter and later work their way through their adult lives. Unfortunately, taking financial literacy courses cannot substitute for the structural changes needed to close the racial and gender gaps in employment, earnings, and wealth that have historically defined and, still today, define our society and economy.